A borrower’s personal finances indicate where their interest rate will fall within the context of this average interest rate.

Fed rate cut. are they good or bad for home buyers?

You can count on it. When the Federal Reserve changes its interest rate, headlines about mortgage rates will follow.

This cycle unfolds up to eight times a year, so many homebuyers get the idea that the Fed regulates mortgage rates.

The Fed’s decisions affect mortgage rates, but the Fed does not directly control mortgage rates. Actually, how? Better It is discussed here that the Fed’s actions can have unpredictable effects on the rates that new home buyers pay on their mortgages.

Does the Fed set mortgage rates?

Federal Reserve It is the most powerful financial institution in the United States, and its decisions affect the entire world economy, including the mortgage market.

When? The Fed adjusts ratesit changes the Federal funds rate, which is the overnight rate that banks charge each other when they provide reserves to manage their cash flows. This interest rate affects the economy’s short-term borrowing costs, including credit card rates, auto loan rates, and home equity lines of credit (HELOCs).

But 30-year fixed mortgage rates are long-term rates. They are largely shaped by the broader financial markets, not by the Fed’s policy committee.

What’s Really Driving Up 30-Year Mortgage Rates?

Mortgage rates are closely related.

- USA: Treasury yieldsespecially the 10-year Treasury.

- The price of mortgage-backed securities (MBS).

- Inflation and jobs data.

- Predictions about future economic growth.

- Demand for US bonds around the world.

- Risk premiums required by investors.

All of this affects mortgage rates because a home loan does not exist in an economic vacuum. After a borrower closes on a mortgage to purchase a primary residence, the lender often sells the loan on the secondary market.

Multiple mortgages are combined into mortgage-backed securities, financial assets that investors can buy and sell. Investors who buy mortgage-backed securities expect a return that offsets inflation risk, interest rate risk, and potential borrowers refinancing sooner than expected.

Because of this expectation, mortgage rates come with future risks and rewards already included in their pricing. This month’s home loan rate reflects what investors think will happen with inflation, economic growth and Fed policy over the next few years.

How do mortgage rates react when the Fed lowers its interest rate?

When the Fed lowers the federal funds rate, as it did three times between September and December, many borrowers expect mortgage rates to drop immediately. Sometimes interest rates fall, but not always.

It is one of the reasons. mortgage markets are usually priced into a Fed tapering before that happens.

If investors expect the Fed to cut interest rates, they react to that expectation before it happens. That’s why Treasury yields and mortgage rates often fall before an official Fed announcement.

When the Fed does act, mortgage rates may barely move, or may even rise if the cut is smaller than markets expected.

Why mortgage rates sometimes rise after Fed tapering

Mortgage rates could rise after a Fed rate cut if:

- Inflation still looks persistent.

- Employment data is strong.

- Investors expect interest rates to rise again in the future.

- Bond markets sell off due to high demand for stocks.

When one or more of these market forces converge, investors can expect higher long-term bond yields. This raises mortgage rates even as short-term interest rates fall.

The Fed chairman’s comments on the future of the economy could also cause mortgage interest rates to rise.

For example, after 0.25% cut in OctoberFed Chairman Jerome Powell said more cuts in December are not a foregone conclusion. Markets responded with a temporary rise in mortgage rates despite the Fed’s rate cuts.

Again, mortgage rates reflect the future outlook of the economy, not its current conditions.

Will mortgage rates continue to fall on the back of Fed tapering in 2025?

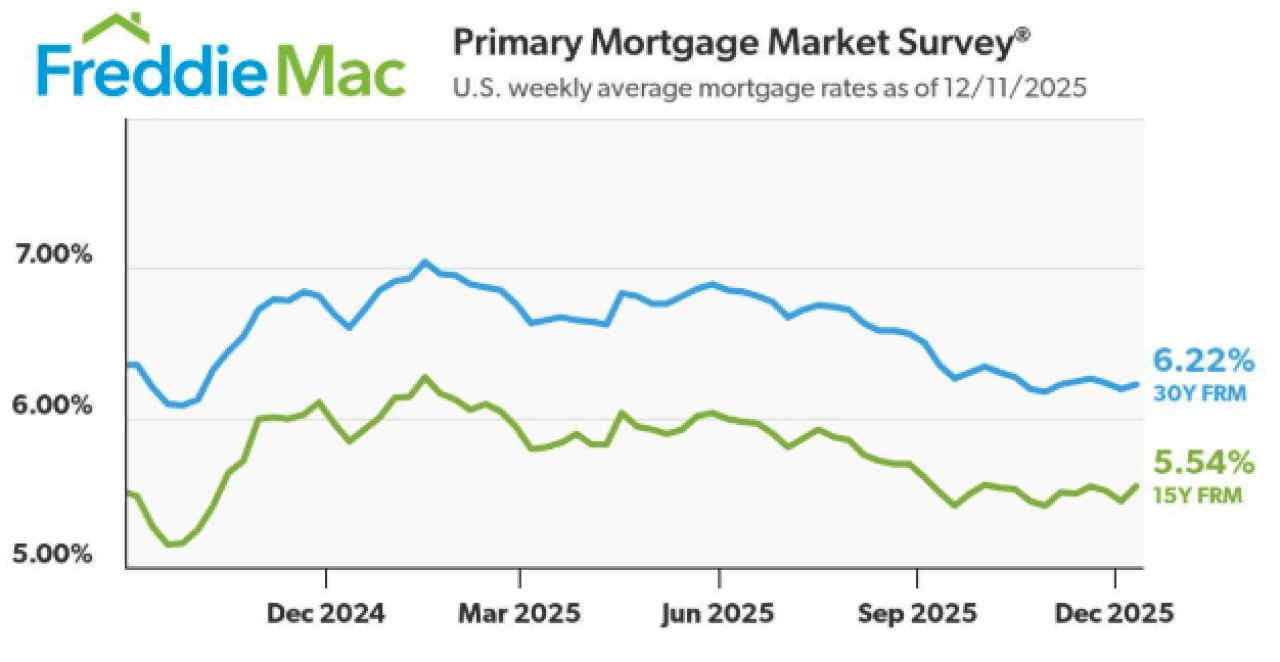

The Federal Reserve cut the federal funds rate by 0.25% three times in the last four months of 2025. Investors anticipated each of these cuts, and every time Fed governors met, they were right.

In the months leading up to the Fed’s rate cut campaign in late 2025, mortgage rates had already started to fall as investors priced in slower economic growth. By the time policymakers acted, much of the impact had already been absorbed by financial markets.

This dynamic helps explain why mortgage rates did not fall sharply even as the Fed cut its benchmark interest rate by a total of 0.75% between September and December.

As for 2026 Many economists believe rates could continue their gradual decline, possibly falling below 6% for the first time since September 2022. Of course, no one knows what future economic changes could change these predictions.

How do rates and other volatility affect mortgages?

Mortgage rates follow a reasonably predictable cycle;

- A strong economic outlook is driving up mortgage rates.

- A weak economic outlook is putting downward pressure on mortgage rates.

How mortgage rates respond to uncertainty about the future is harder to explain, and uncertainty has been a hallmark of the 2020s.

First, the COVID-19 pandemic interrupted what could have been a period of rising mortgage rates in 2020 and 2021. Instead, as the economy shut down, mortgage rates hit historic lows. Inflation then set in, punctuating the Fed’s aggressive rate hike campaign in 2022 and 2023.

Now, under the second Trump administration, Tariffs added upward pressure on pricescausing concern about inflation.

If investors believe rates will keep inflation above the Fed’s target, mortgage rates could stay roughly the same even during the Fed’s rate-cutting cycle, which is currently underway.

Along with tariffs, economic instability can come from several areas.

Labor market and wage growth

Strong wage growth is good for households, but it can also worry bond markets.

If wages rise faster than productivity, the risks of inflation increase. This could keep mortgage rates high regardless of what the Fed does in the short term.

Government borrowing and supply of bonds

Large federal deficits translate into more bond markets. This increased supply can increase yields. Under these conditions, mortgage rates often rise in tandem with Treasury yields.

Global instability

Foreign investors also influence US mortgage rates. Economic instability abroad could push more money into the relative safety of U.S. bonds, driving down mortgage rates. Strong global growth could drain capital from US bonds, pushing up interest rates.

What will happen to mortgage rates in 2026?

No one can predict mortgage rates with certainty, but we can focus on the forces that are likely to shape interest rates.

If economic growth freezes in 2026.

- Inflationary pressures may weaken.

- Bond yields may fall.

- Mortgage interest rates may gradually decrease.

This may represent a normalization scenario rather than a sharp drop in rates.

Why is a return to extremely low interest rates unlikely?

The sub-3% mortgage rates seen at the start of the decade were the result of unusual conditions;

- Near zero short term rates.

- Fed’s massive bond buying programs.

- Economic shocks due to the epidemic.

Unless we experience a major recession or financial crisis, mortgage rates are unlikely to return to those levels.

What does all this mean for borrowers?

How do everyday home buyers navigate this global tapestry of forces shaping mortgage rates? Rarely reacting to Fed moves, no matter what the headlines say.

Instead, homebuyers and refinancing homeowners can build their affordability by controlling what they can control: their personal finances.

News outlets report average mortgage interest rates. A borrower’s personal finances indicate where their interest rate will fall compared to this average rate.

Borrowers:

- Larger down payments (or more home equity for refinancers)

- Higher credit scores

- Lower monthly payments

- Work stability

These borrowers can often qualify below average mortgage ratesresulting in lower monthly payments.

A: mortgage calculator helps borrowers see how a monthly mortgage payment works out.

A mortgage pre-approval can show how your personal finances work with global economic forces to shape your interest rate.

This story was produced Better and revised and distributed Stacker.

RELATED CONTENT: Alvin Ailey’s American Dance Theater enters the final weeks of the New York holiday season; A 2026 national tour has been announced